Why is Everything Racist?

Housing Explains Woke Pseudo-Racism

I wrote this after reading Richard Hanania’s essay “Why is Everything Liberal?,” which argues that all major institutions are woke because liberals invest more time and effort in their causes.

In America, we are supposed to hate racism. Our nation was founded with the principle of individual liberty enshrined in our Bill of Rights and our Pledge of Allegiance is an oath to the Republic “with liberty and justice for all.”

You might even think we are doing rather well at combatting the problem. We had the abolitionist movement, the Civil War, the Civil Rights movement, the Black Power movement, the Anti-Apartheid movement and the Black Lives Matter movement. Our laws and court decisions include the Fourteenth Amendment, the Fifteenth Amendment, Brown v. Board of Education, the Civil Rights Act, the Voting Rights Act, the Fair Housing Act and the Fair Sentencing Act, to name but a few.

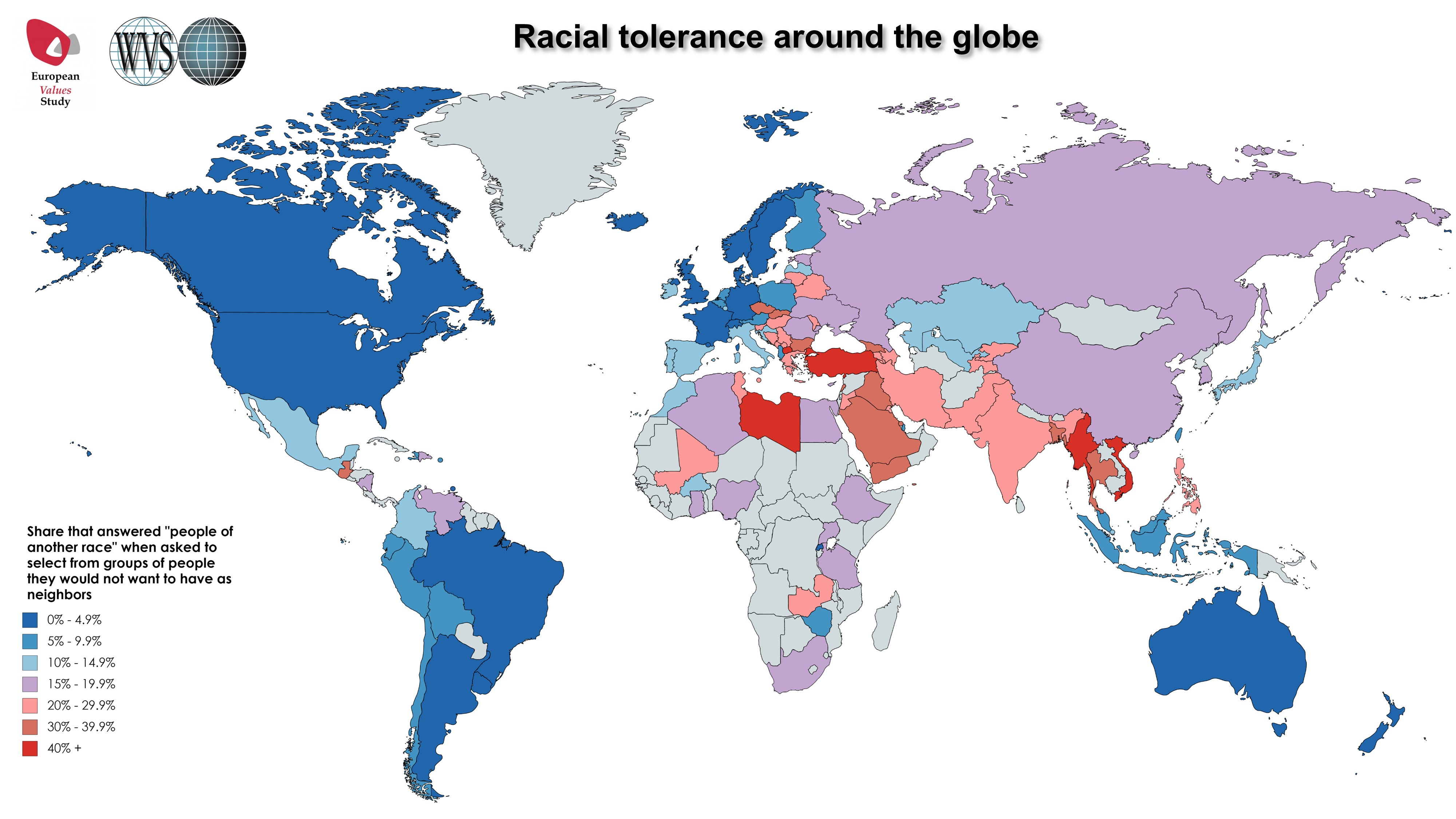

The updated 2020 version of the World Values Survey found the U.S. to be one of the least racist countries in the world, based on the share of respondents who answered “people of another race” when asked to select from groups they would not want as neighbors. Other options included drug addicts, people who have AIDS, immigrants, homosexuals, people of a different religion, heavy drinkers, unmarried couples living together and people who speak a different language.

Yet if you listen to the public discourse, you would get the impression that our society is utterly soaked in racist hatred. Our words and phrases, logos and mascots, statues and monuments, films and songs are all apparently dripping with it. But a careful observer will quickly notice the accusation of racism often rings false. Some of the things deemed racist include Mark Twain’s anti-racist classic “The Adventures of Huckleberry Finn,” the children’s cartoon “The Flintstones,” milk, peanut butter and jelly sandwiches, daylight savings time, even trying not to be racist.

There is a natural tendency to dismiss all this as hysterical oversensitivity. But I think it’s worth tracing the history of this phenomenon.

It wasn’t always the case that everything was labeled racist, and aside from being dumb and annoying, these accusations of racism, or more accurately pseudo-racism, diminish the degree to which people take such charges seriously, which does real harm to the very people such accusations are meant to protect. So why is everything racist?

Home Sweet Home

In the land where dreams are made, the American dream is all about owning a home. Early settlers saw owning land and a home as a means of freedom. This was the allure of the New World—to kindle the flame of self-reliance and cultivate one’s own patch of earth, and with it, one’s destiny.

This was also the allure of the West. The Homestead Act of 1862 encouraged westward expansion by offering 160 acres to settlers so long as they improved the land by building a home and growing crops. Millions of Americans risked their lives and the lives of their loved ones for the simple dream of a home on the range.

The Oregon Trail migrations of the 1840s and the California Gold Rush from 1848 to 1855 drew vast waves of settlers. But the final nail in the coffin of this era of American life was a literal one—the driving of the Golden Spike at Promontory Summit in Utah in 1869, marking the completion of the First Transcontinental Railroad. Millions more could suddenly reach the Pacific while scarcely looking up from their newspapers and the U.S. Census Bureau declared in 1890 that the frontier no longer existed.

But the agrarian life of the common American continued throughout the 19th century. The average home, especially out west, remained a simple log cabin. Simple though it was, this structure and the land on which it sat was the most powerful symbol of success and social standing in the country, and the most valuable thing a family could pass on to future generations. There was no electricity, no indoor plumbing and no central heating. If you wanted fire, you had to cut wood. If you wanted water, you had to draw it from the well. It was rough and simple living, but it was home.

That was the first major inflection point in the evolution of homeownership across the grand sweep of American history. During the Colonial Era, owning a home had been the domain of wealthy landowners while most folks were renters or indentured servants. The Homestead Act was therefore a clarion call of freedom open to those who could coax life from the soil and erect a hearth. It painted the canvas of the American tableau with a broader brush and further democratized the American dream.

There were only four more inflection points following this. One was the Industrial Era, in which the 19th century bore witness to a great shift from the rustic life of log cabins to urban living. Also during this time, the modern mortgage system began to take shape. The establishment of savings and loan associations and the use of fixed-rate mortgages made homeownership more accessible.

The next inflection point came after World War II when the GI Bill provided veterans with low-interest mortgages. This made homeownership still more accessible and the era of suburbanization that followed led to a surge in single-family houses. But redlining, educational disparities and discrimination in the distribution of veterans’ benefits worsened the racial wealth gap. So as the American dream became ever more attainable, it was pulled further from the reach of black Americans.

The next inflection point came after the Civil Rights movement. The Fair Housing Act, signed into law by President Lyndon B. Johnson in April 1968, made it illegal for landlords to refuse to sell or rent housing on the basis of race, religion, nationality, sex, disability or family status. It also made discriminatory advertising illegal as well as the practices of “steering,” or directing unwanted people away from certain neighborhoods, and “blockbusting,” or getting folks to sell property at lower prices, usually by telling them blacks were moving into the area.

Each of these four inflection points made homeownership more accessible for more Americans. This was great because homeownership is not merely a symbol of freedom or equal standing. It also contributes to the economy through construction and real estate. It serves as collateral for loans. It forms neighborhoods that provide a sense of community and shared belonging. So you can imagine that a major disruption would have profound impact not just on our economy but on our sense of identity and the contours of our political landscape. And that’s exactly what happened in 2008.

The Dream Within Reach

The first four inflection points were positive, but the fifth was a disaster ironically brought on by unprecedented success. Homeownership increased through the 1970s, faltered slightly in the late 1980s, then soared to a staggering 69.2% in 2004, according to data from the U.S. Census Bureau. This penciled out to 76% for whites and 49.1% for blacks. That’s largely the result of the legacy of slavery and Reconstruction Era racism, plus the discriminatory practices outlined above, as well as other factors including the bundling of housing and labor markets and subsequently unattractive commutes.

Nevertheless, homeownership has remained the American dream. According to a survey of 2,529 adults released in March 2022 by the financial services company Bankrate:

Owning a home is still very much a part of the “American Dream,” as cited by 74% of U.S. adults. This is more than those who point to being able to retire (66%), having a successful career (60%), owning a car, truck, or other automobile (50%), having children (40%), and getting a college degree (35%). Younger adults are less likely to feel this way, however, with 59% of Gen Z and 65% of millennials selecting homeownership compared to 78% of Gen X and 85% of baby boomers.

People long for the safety, the quiet, the yard where their kids can play and the white picket fence. Those who can afford to buy homes happily do so and those who cannot happily assume debt to make it work. By the third quarter of 2008, household debt had ballooned to a mind-boggling $12.68 trillion. The American dream was finally within arm’s length. But by stretching out to grasp it, we fell headfirst over the edge of a cliff.

A Perfect Storm

The housing market was hotter than Black Rock Desert in the summer. The Federal Reserve was playing with interest rates like a DJ at Burning Man and real estate agents were dancing in the sun, ignoring the growing number of people collapsed from heat exhaustion. Consider this 2008 paper by Harvard’s Joint Center for Housing Studies:

Subprime mortgages rose from only 8 percent of originations in 2003 to 20 percent in 2005 and 2006, while the interest-only and payment-option share shot up from just 2 percent in 2003 to 20 percent in 2005.

Meanwhile, home prices skyrocketed. In 2010, Forbes reported:

Homes in New York now cost 91% more per square foot than they did in 2000. Los Angeles and Washington, D.C., weren't far behind, rising 85% and 72%, respectively.

There’s no need to rehash the entire crisis. As we now know, of course, it was a house of cards made up of a delicately balanced housing bubble, subprime mortgages bundled into mortgage-backed securities and collateralized debt obligations, opaque financial derivatives such as credit default swaps, corrupt rating agencies and a lack of sufficient regulatory oversight. The housing market collapsed and by 2016 homeownership was down from 69.2% to about 63%.

We survived, but we were never the same. Since 2008, the median cost of a home has risen dramatically in most states, and nearly doubled in almost a dozen. Among other things, supply-chain disruptions and the subsequent lack of available lumber and other supplies has led to sharp increases in the cost of a new home. Suddenly, for millions of people the great American dream of homeownership had slipped away.

President George W. Bush signed the Economic Stimulus Act of 2008, which among other things created the Federal Housing Finance Agency. Bush also initiated the Troubled Asset Relief Program (TARP). In 2009, President Barack Obama signed the American Recovery and Reinvestment Act, a $787 billion stimulus package. But it was highly controversial, giving Republicans the boost they needed to take the House in 2010 and partly giving rise to the Tea Party movement, which in turn contributed to the election of Donald Trump in 2016.

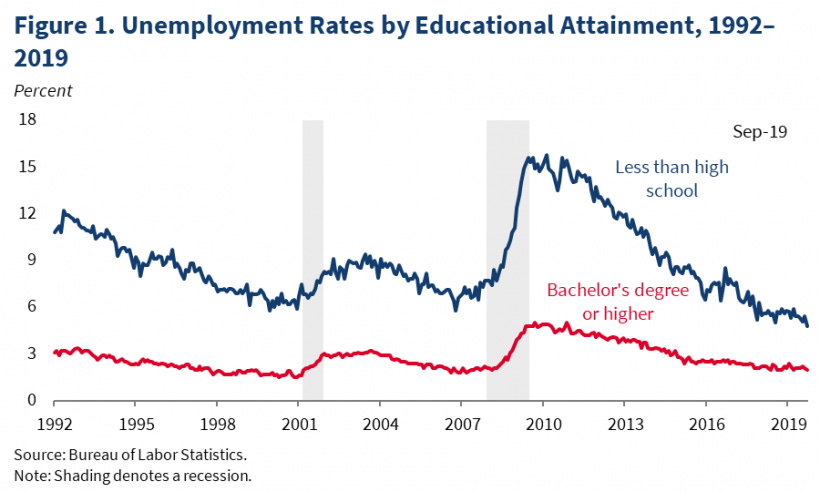

The unemployment rate also rose precipitously from 5% in 2007 to 10% in 2009. This was the result of the housing market crisis but also banks and financial institutions that tightened lending standards in response to the crisis, as well as overall global economic uncertainty. It took years for the U.S. to bring its unemployment rate back down to something normal, and we did not get below 5% until the second quarter of 2016 when we hit 4.9%. But 2016 was disruptive for other reasons, namely the controversy-chasing presidential campaign and election of Trump.

Then we were hit by the Covid pandemic, the killing of George Floyd and the Black Lives Matter protests. We saw downtown areas set ablaze and small businesses smashed open while at the same time progressives argued we needed to “defund the police.” In one salient example, downtown Seattle became overtaken by violent Antifa protesters and local officials essentially threw up their hands and walked away.

Hilary Clinton became the new face of the Democratic Party but many were turned off by what they perceived as a sense of entitlement. It was her time, everyone kept saying. It also did not help that her husband had signed NAFTA into law in 1993, which many blamed for significant job losses. On the other hand, Bush had just waged broadly unpopular wars in Afghanistan and Iraq and despite significant tax cuts—the Economic Growth and Tax Relief Reconciliation Act of 2001 and the Jobs and Growth Tax Relief Reconciliation Act of 2003—he increased government spending and national debt went up by more than 105%, a greater increase than under any president since Reagan.

As a result, both parties looked like big-spending, war-mongering organizations catering to elites at a time when many Americans had never had it harder. We were all grinding our teeth over the cost of housing and the nation’s job markets, everyone on on edge, when we got pummeled with a pandemic and a racial reckoning and the amplifying effects of social media. So yes, we lost our chill.

The left ended up claiming all sorts of things were racist, even things that definitely were not, while the right ended up dismissing claims of racism, even for things that definitely were. The progressive left went woke and the reactionary right went MAGA and we’ve been in a doom spiral ever since.

Things will get worse before they get better. But to get better, both sides need to put down the knife and return to basic solutions to simple problems. In politics, so much comes down to one thing—it’s the economy, stupid. What we see on the far-left and far-right are often emergent manifestations of insecurity. That’s not the whole explanation, but give someone a job so they can buy a home and watch their shoulders sink an inch.

Westward Expansion required the vilification, often violent subjugation, and relocation of an entire race of people. "Kill the Indian in him, save the man" was a guiding principle, sometimes even an offical practice. Have Native American lives greatly improved since then? Absolutely. Do we face less racism? Yes. Are our lives still beset by the legacies of colonial rule? Also, yes.

Can it really be called home "ownership" when the bank owns the home for the next 30 or so years? When you have to pay an extra fee on the mortgage creatively named "insurance" until you have 20% equity in the home as the vast majority of home buyers do? When many people don't realize that PMI is supposed to stop after 20% of the supposed value of the house is paid for and the bank keeps charging it anyway? When even after the house if fully paid for after 30 years (likely in retirement) and you still owe property taxes? When the government can increase those taxes so much that you can no longer afford "your" property?

Does it really matter if you make out your monthly checks to a landlord as rent or to the bank as mortgage? You still owe money to someone for the privilege of living in "your" space. That someone will take "your" space back if you fall behind on those payments. And that includes the government if you can't afford the property taxes.

It's a nicely written article with a number of fair points. However, I don't think that home ownership should be the metric we use to determine financial success unless we consider home ownership to mean actually fully paid off mortgages and affordable property taxes (affordable on retirement savings or social security payments). Mortgages and debt (student loans, car loans, credit card debt, etc) are just another way that the elite can subjugate the poor, in my opinion. You can't be free if you owe your soul to the company store (or the bank).